Welcome to my blog about investing in Japan.

Japan is one of the world’s largest equity markets, with deep capitalization, an unusually high share of manufacturing and industrial names, and a distinctive corporate culture that shapes returns. For an investor, there are many opportunities, but also pitfalls.

In this article, we will take a look at some of the specific opportunities, mechanics, and frictions that you may encounter as you approach the Japanese economy from an investor’s perspective. We will chiefly, but not exclusively, look at the stock market and how to gain exposure to Japanese stocks. Read on if you want to find out more about how the market is structured, which indices that are available, how to get access from inside or outside Japan, tax and settlement realities, broker and custody considerations, sectoral peculiarities, and more.

Japanese corporate governance has been an active policy focus for several years. Reforms encouraging higher shareholder returns, independent boards, and clearer disclosure have changed the behavior of many firms and contributed to higher aggregate dividends in recent cycles. That shift matters because it has reduced one traditional discount that Japanese stocks carried. There used to be a tendency to hoard cash and under-reward shareholders. For investors this means total return can come from both capital appreciation and rising dividends. It also means engagement with management and attention to governance metrics can be a productive part of security selection. This is not universal, and company-level analysis remains essential, but the broad direction has improved investor rights and transparency, especially among larger Prime-market firms.

Daytrading Japanese stock

There are a number of different US and UK brokers that offer CFD:s and other financial instruments based on Japanese stocks. This makes it easy to day trade and make leveraged trades on the Japanese stock market. Day trading in Japan can extend the number of hours you can trade each day since the Japanese market is open during other times then the US and European markets. Extending the number of hours you can trade each day can dramatically improve your profits but can also cause you large loses if you trade for longer periods than you are able to stay alert. Never keep trading if you are too tired to make good choices.

How to gain exposure to Japanese equities

The four main paths to exposure for foreign investors:

- Buy listed shares directly on a Japanese exchange through a broker.

- Buy ADRs representing shares of a Japanese company.

- Buy Japan-focused ETFs or mutual funds.

- Gain indirect exposure through global companies with heavy Japanese revenue.

Buying direct on JPX gives you the cleanest exposure and access to corporate actions and shareholder meetings, but requires a broker that can clear and custody Japanese securities. ADRs are available in the United States, and can be easier to use for retail investors abroad when it comes to settlements, currency conversion, and reporting.

ETFs work if you don´t want to pick individual stock companies. They can simplify rebalancing and diversification. If you want a passive, low-maintenance allocation, ETFs are typically the most efficient route.

These are not the only ways to gain exposure, just four examples of common choices among investors.

Risks and considerations before you invest in Japanese companies

Examples of country-specific risks deserve attention.

- Cross-shareholdings historically reduced float and could dampen takeover activity, although reforms have reduced this effect.

- Demographic trends and slow GDP growth create long-run structural headwinds for domestic consumption, though corporate returns and shareholder policies can offset this.

- Currency volatility can produce surprising portfolio swings for foreign investors. Yen moves can materially affect USD-based returns. Decide whether you want unhedged yen exposure (which adds return volatility) or hedged exposure (which reduces currency risk but adds cost).

- Liquidity can be thin on smaller names and mid-cap and small-cap stocks. This widens execution costs, and increases price impact for larger orders. Execution and custody choices can become especially important as you move down market-cap tiers.

- Legal and disclosure norms may differ from what you are used to. Some governance and disclosure practices that foreign investors expect may not be identical, so factor that into your research approach.

- Dividends and tax. If you’re non-resident, dividend withholding and treaty relief rules matter. Residents can use local tax-advantaged accounts where available. Confirm the tax treatment for dividends, capital gains and any local withholding before you commit.

- Valuation vs cyclical exposure. Many Japanese large caps look cheap on headline multiples relative to global peers because of sector composition and conservative corporate balance sheets. That cheapness often reflects cyclical risk (autos, capital goods) rather than structural weakness. Consider earnings cyclicality and global capex trends when sizing positions.

- Corporate governance and shareholder returns. Japan has undergone governance reforms that encouraged higher dividends, share buybacks and board independence. That shift is structural and has made investors more interested in Japanese equities for both income and value exposure.

Settlement in Japan

Japan moved to a T+2 settlement cycle in mid-2019, which is now standard. Trades settle two business days after execution. Settlement timing matters for cash management, for dividend entitlement dates, and for margin requirements if you trade on leverage.

Stock exchanges in Japan

There are currently five stock exchanges in Japan. The two national stock exchanges are Tokyo Stock Exchange (TSE) and Osaka Exchange (OSE). The other three are regional exchanges.

- Tokyo Stock Exchange (TSE) Japan’s largest and most important stock exchange. Operated by the Japan Exchange Group (JPX), it includes multiple market segments such as Prime, Standard, Growth, and the TOKYO PRO Market.

- Osaka Exchange (OSE) Also operated by the Japan Exchange Group (JPX), the Osaka Exchange primarily focuses on derivatives, including futures and options, rather than cash equities.

- Nagoya Stock Exchange (NSE) Based in Nagoya, the Nagoya Stock Exchange serves companies mainly in central Japan. It has its own listings in addition to TSE dual listings.

- Fukuoka Stock Exchange (FSE) Located in Fukuoka, this exchange focuses on companies in Kyushu and southern Japan. It includes a growth-oriented segment similar to the TOKYO PRO Market, called the “Q-Board.”

- Sapporo Securities Exchange (SSE) Based in Sapporo, this is the smallest of Japan’s stock exchanges and primarily serves Hokkaido-based companies.

The Tokyo Stock Exchange (TSE)

The Tokyo Stock Exchange (TSE) is Japan’s largest and most significant stock exchange. It is operated by the Japan Exchange Group (JPX), which also manages the Osaka Exchange. The TSE is a central hub for both domestic and international investors seeking exposure to Japanese equities. The exchange is known for its extremely high trading volumes, especially for large-cap stocks. Foreign investors can access through brokers.

As the core of Japan’s capital markets, movements on the TSE influence global indices and investor sentiment in Asia. It is actually one of the largest stock exchanges in the world, making it a key venue for international capital flows, and it hosts the majority of Japan’s publicly listed companies, including global giants like Toyota, Sony, and Mitsubishi UFJ Financial Group.

TSE has multiple tiers:

- Prime Market: Large, established companies meeting strict governance and liquidity standards.

- Standard Market: Mid-sized companies with moderate requirements.

- Growth Market: Emerging companies with higher growth potential.

- TOKYO PRO Market: Specialized segment for professional investors and innovative companies.

The TSE follows a two-session trading schedule (all times in Japan Standard Time, JST):

- Morning session: 9:00 AM – 11:30 AM

- Afternoon session: 12:30 PM – 3:00 PM

Pre-market and after-hours trading:

- Pre-open sessions occur before 9:00 AM for order placement and price discovery.

- Some limited post-market trading occurs in the evening session for special programs or derivative products.

As for all exchanges, session timings and holiday calendars matter because they determine when orders execute, when news are priced, and when corporate announcements are released. If you trade from a different time zone you’ll need to plan order execution around these sessions and be aware of how overnight risks can accumulate.

The Osaka Exchange (OSE)

The Osaka Exchange, Inc. (OSE) is Japan’s primary derivatives exchange. It specializes in equity index futures and options, interest rate products, and some commodity derivatives.

Today, OSE operates as a subsidiary of the Japan Exchange Group (JPX), alongside the Tokyo Stock Exchange (TSE). OSE was founded in 1878 and merged into JPX in 2013. OSE is located in Osaka, the city which together with Kobe and Kyoto forms the Keihanshin Metropolitan Area, the second-largest urban area in Japan. Osaka has a very long history of being a commercial and merchant hub, and in the late 1600s CE, merchants here started trading forward-style rice contracts at the Dōjima Rice Market. These contracts represented future delivery of rice and were used to manage price risk, very similar to modern futures.

OSE is best known as the trading venue for Nikkei 225 futures and options, TOPIX futures and options, JPX-Nikkei 400 derivatives, JGB (Japanese Government Bond) futures, and volatility and interest rate derivatives. The Nikkei 225 futures are one of the most traded equity index futures in Asia and they are widely used by global hedge funds, asset managers, and macro traders. The Nikkei 224 options are key tools for volatility trading and downside protection.

OSE products are widely used to hedge Japan equity portfolios, manage yen-linked equity risk, and implement macro and relative-value strategies. OSE contracts trading overlap with Europe and the U.S. via extended session. All contracts are yen-based.

The stock indices Nikkei 225 and TOPIX

The two headline indices are the Nikkei 225 and TOPIX. The Nikkei 225 is a price-weighted basket of 225 large, liquid stocks selected from the Prime market and it often headlines news because of its long history and concentrated format. TOPIX, by contrast, is a capitalization-weighted index covering the First/Prime market and is a broader benchmark for the whole market. Understanding the difference matters because a large, high-price stock can move the Nikkei disproportionately while TOPIX reflects market capitalization more directly. Many institutional funds and ETFs are constructed against one index or the other so your choice of benchmark will influence exposures.

About Nikkei 225

The Nikkei 225 is Japan’s most well-known stock market index. This price-weighted index tracks 225 large, liquid companies listed on the Tokyo Stock Exchange (TSE) and is often compared to the Dow Jones Industrial Average in the U.S.

Established in 1950, this index covers blue-chip Japanese companies across multiple sectors. It is denoted in yen. Examples of well-known constituents are Toyota, Sony, SoftBank Group, Keyence, Fast Retailing (Uniqlo), and Nintendo. The Nikkei 225 is often viewed as a barometer of Japan’s large-cap corporate sector and a proxy for export-driven and technology-oriented Japanese firms. For traders, it is frequently used to gain exposure to the Japanese economy. The Nikkei 225 is especially sensitive to global trade conditions, the strength of the yen, and technology and industrial cycles. A weaker yen often boosts profits for Japanese exporters and can lift the index.

International investors typically access the Nikkei 225 via ETFs, futures, options, or mutual funds. ETFs are available in both currency-hedged and unhedged versions.

Before investing, it is important to take into account that the Nikkei 225 is a price-weighted index, so high-priced stocks have outsized influence. A company’s stock price matters more than its actual size, and this will impact performance and risk exposure. The index is heavy in industrials, consumer electronics, and technology, and light in financials and services compared to Japan’s broader economy. Compared to the TOPIX, the Nikkei 225 is less representative of the full Japanese economy. While not exclusively an index for large-cap only, it underrepresents small- and mid-cap growth companies.

About TOPIX

TOPIX (Tokyo Stock Price Index) is Japan’s primary broad-market equity index. It includes nearly all domestic common stocks listed on the Tokyo Stock Exchange Prime Market, making it the most representative measure of the Japanese equity market. Unlike Nikkei 2254, TOPIX is free-float market-capitalization weighted.

TOPIX covers roughly 1,700 companies, and the exact number varies with rebalancing. The index was launched in 1969 and the currency is JPY. TOPIX is often compared to the S&P 500 in terms of structure and representativeness.

TOPIX represents both export-oriented and domestically focused companies, and the sector exposure is aligned with Japan’s real economy. The index is widely used by pension funds, institutional investors, and long-term global allocators.

Just as with the Nikkei 225, investors can gain exposure to TOPIX in various ways, including ETFs, mutual funds, and index futures. If you don´t want Japan-listed ETFs, ETFs tracking TOPIX are available on European and U.S. stock exchanges as well.

Because of the market-cap weighting, banks and financial institutions have significant influence on TOPIX, and performance can lag during low interest-rate periods. There is also more exposure to slower-growth domestic companies (compared to Nikkei 225), such as utility companies, railways, retailers, and regional banks. The higher inclusion of companies more exposed to Japan’s aging population and low growth can also dampen overall returns. TOPIX has lower volatility than the Nikkei 225, is less sensitive to global tech and exporter cycles, and may underperform during sharp global risk-on rallies. The large number of constituents dilutes the impact of standout performers, and for some investors, TOPIX is not exciting enough.

TOPIX tends to be favored by investors look for core, long-term exposure to Japan,

portfolio builders who want structural consistency with global indices, and investors preferring broad diversification over tactical bets. The index is less suitable for short-term trading strategies (low volatility), investors focused purely on exporters or tech, and investors seeking concentrated upside.

Japanese stock index groups – find the right index for your objectives

Japan’s equity indices are often grouped according to their role, coverage, and how investors use them. Each group serves a distinct purpose in market analysis and portfolio construction. This grouping framework helps investors and analysts understand what part of the Japanese market an index represents. i.e. whether it is a broad market barometer, a large-cap benchmark, a quality-focused selection, a size-specific segment, or a growth-oriented universe.

Headline indices

The above-mentioned Nikkei 225 and TOPIX are both headline indices that serve as primary indicators of Japan’s stock market performance. They are also the Japanese indices most frequently cited in global media. As you know, the Nikkei 225 is a price-weighted index of 225 highly liquid, well-known companies, and is widely used by international investors as a shorthand for “the Japanese market,” even though it does not represent the entire market. TOPIX, by contrast, is market-capitalization weighted and covers nearly all domestic stocks listed on the Tokyo Stock Exchange Prime Market. This makes it the most comprehensive and representative benchmark of Japan’s equity market, and institutional investors often prefer TOPIX because it reflects the market as a whole rather than a selected subset.

Size-segmentation indices

Size-segmentation indices are stock indices that classify and track companies based on their market capitalization. Instead of trying to represent the entire market or only the largest companies, these indices divide the market into large-cap, mid-cap, and small-cap segments, allowing investors to focus on performance by company size. In Japan, these indices are mainly derived from TOPIX (Tokyo Stock Price Index).

Investors looking for large-cap indices often go for the TOPIX Core 30 and TOPIX Large 70, since they focus on Japan’s largest (by market cap) companies. TOPIX Core 30 consists of the country’s biggest blue-chip firms. These are companies that dominate their industries and attract the majority of foreign investment flows. It is often used to track the performance of Japan’s corporate giants. TOPIX Large 70 expands this universe to include 70 large-cap stocks, offering broader exposure while still maintaining the strong large-company focus. Both of these indices are useful for investors who want to isolate large-cap performance from the rest of the market.

TOPIX Mid400 tracks mid-capitalization companies, which are often more growth-oriented than large caps but still well-established and liquid. As the name suggests, it tracks 400 mid-sized companies. Historically, mid-cap stocks in Japan have higher growth potential than large-caps, though with slightly higher risk. They tend to outperform during economic recoveries but may underperform large-cap indices during market downturns.

TOPIX Small is for small-cap companies, which tend to be more sensitive to domestic economic trends and can offer higher growth potential, along with higher risk. As of the end of 2025, the TOPIX Small index included 1,167 companies. TOPIX Small is defined as all TOPIX constituent stocks that are not in the TOPIX 500 index (which itself covers the largest 500 stocks).

Style & quality indices

Style & quality indices are designed to track companies with strong corporate governance, profitability, and efficient management, rather than simply the largest or most heavily traded firms. These indices aim to highlight “quality” companies that are financially healthy, well-governed, and likely to deliver sustainable returns over time.

In Japan, the primary example of this type of index is the JPX-Nikkei 400. The JPX-Nikkei 400 is designed to emphasize corporate quality and governance, not just size. Its constituents are selected based on criteria such as profitability, return on equity, and disclosure standards, alongside market capitalization and liquidity. This index is frequently used as a benchmark for strategies focused on efficiency, shareholder returns, and governance improvements in Japanese companies.

The JPX Nikkei Index Human Capital 100 is a subset of the JPX Nikkei 400 that tracks 100 companies with strong human capital focused management practices, scoring firms on workforce development and disclosure.

The JPX Nikkei Mid and Small Cap Index is not only size-segmented; it also applies quality screens (profitability/ROE) to select mid and small cap firms demonstrating efficient management.

Growth-focused indices

Growth-focused indices are designed to track young, innovative, and fast-growing companies rather than mature, established corporations. In Japan, these indices mainly cover firms listed on the Tokyo Stock Exchange (TSE) Growth Market, which was created to support startups and emerging businesses with high growth potential. Growth-focused indices in Japan are used as a benchmark for Japan’s venture and innovation segment, as they allow investors to measure how early-stage and growth companies are performing as a group, separate from large-cap and traditional industries that dominate indices like TOPIX and Nikkei 225. These indices are often used by venture capital–oriented investors, growth equity funds, retail investors seeking higher return potential, and analysts tracking innovation trends in Japan.

Companies in growth-focused indices tend to share several characteristics, including small market caps and being recently listed. High reinvestment rates are common, with profits redirected toward expansion. Profitability is not always required for inclusion in a growth index, as business scalability and growth prospects are more important. Growth-focused Japanese indices typically exhibit much higher volatility than TOPIX or Nikkei 225, stronger performance during risk-on markets and economic recoveries, and sharpened drawdowns during market stress or rising interest rates. Because many constituents are still scaling their businesses, valuations can be sensitive to changes in sentiment, funding conditions, and technology cycles.

Examples of well-known Japanese growth indices are the TSE Growth Market Index and the TSE Growth Market 250 Index (formerly the Mothers Index). The TSE Growth Market Index is a broad benchmark covering the TSE Growth Market as a whole. It is generally seen as the main performance gauge for Japanese growth stocks. TSE Growth Market 250 Index focuses on 250 representative growth companies from the TSE Growth Market. It is more liquid and investable than the broader Growth Market Index, and is widely used for ETFs and structured products. The index focuses on 250 representative companies, rather than the hundreds of small- and micro-cap firms in the broader Growth Market Index. By selecting the most tradable and financially stable growth companies, it naturally includes stocks that are actively traded on the TSE. Less illiquid, thinly traded micro-cap stocks are excluded, which reduces transaction costs and price slippage. Higher liquidity means that investors can buy or sell larger positions without significantly moving the price, and ETFs, mutual funds, and structured products can track the index more accurately.

Growth-focused indices play an important role in showing where Japan’s future growth may come from, beyond its traditional manufacturing and export giants. They complement broader benchmarks by capturing innovation, entrepreneurship, and structural changes in the Japanese economy. In portfolio construction, they are often used as a satellite allocation, adding growth potential and diversification alongside core holdings in large-cap or broad-market indices.

Brokers, account types and custody

If you open an account with a Japan-based broker you’ll see product sets and account types tuned to domestic retail clients, including direct market access and tax-advantaged wrappers. Non-Japanese brokers may still offer overseas access to Japanese stock-exchanges, or simply provide access to ADRs and ETFs.

Before committing capital with any broker, confirm where the broker holds client assets, which clearing house is used, and whether the broker provides translated corporate notifications if you do not read Japanese. Also check FX conversion costs if your base currency differs from the yen, because conversion spreads can quietly reduce returns over time. All this might feel like hard and unnecessary work when you are eager to just get started, but you really need to know where your shares are held (local custodian vs offshore omnibus) and how corporate communications are handled. Local custody simplifies participation in shareholder votes and corporate actions. Offshore omnibus custody can be cheaper, but sometimes complicates entitlements and increases the friction if you need to exercise rights or follow a takeover.

Compare total costs for your particular investment plan, including any commissions, exchange fees, clearing fees, FX spreads on conversion to/from JPY, and any account custody charges. If you trade frequently, total per-trade cost and execution quality (slippage, partial fills) will dominate the calculation. If you are a buy-and-hold investor, custody safety, tax reporting, and corporate action processing becomes increasingly important.

Run a small operational test before you even consider scaling. Open a small account or use a small deposit to test deposit, trade execution and withdrawal mechanics. Check whether the broker supports your desired order types, and whether the broker actually supplies trade confirmations and corporate notices in English if you ask for it. Confirm how corporate actions such as rights issues, tender offers, and spin-offs are handled operationally for foreign clients. Some processes require additional documentation and time.

Before making a stock purchase, confirm the company’s listing and ticker, check whether you will hold the Japanese listing or an ADR, verify custody arrangements (local custodian vs omnibus), and understand the timeline for corporate actions and settlement (Japan is T+2). Always document FX conversion rates and keep receipts for tax purposes. For single-name exposure, read recent annual reports and governance disclosures and compare free-float and ownership structures.

You can find a good broker for investing in Japanese stocks by visiting Broker Listings. BrokerListings.com makes it easy to find and compare brokers.

Taxes and tax-advantaged accounts

Tax treatment depends on several factors, including residency and account type. Japan operates tax-advantaged retail schemes, such as the Nippon Individual Savings Account (NISA) and the iDeCo for retirement. That offer exemptions or deferrals on dividends and capital gains within permitted contribution limits, and these programs have been expanded in recent years to encourage household investment and are widely used by domestic investors. For non-resident investors, withholding tax applies to certain domestic source income such as dividends. Typical, statutory withholding rates are subject to adjustment by tax treaty, so the effective rate depends on your country of residence and treaty provisions. Residents should also plan for ordinary income tax and local resident taxes on realized capital gains and dividends, and keep careful records because domestic filings and reporting rules differ from other jurisdictions. It can be advisable consult a specialized tax adviser, since cross-border tax outcomes and treaty relief can alter net returns in significant ways.

Sector character and stock selection nuances

Japan is heavily weighted toward industrials, autos, electronics, machinery, and manufacturing value chains, and these sectors dominate the large-cap indices. Financials and consumer goods also feature prominently, but technology in the narrower US sense (platforms, software monopolies) is less concentrated than in US indices, though hardware and components play a major role. This sector mix creates specific cyclical exposures. Global capex and supply-chain cycles can swing Japanese earnings more than consumer-led markets elsewhere. When picking stocks, consider balance-sheet conservatism, export-sensitivity via the yen, corporate governance quality, and the company’s position in international supply chains. Small and mid-cap stocks can offer higher growth, but often trade with lower liquidity and wider spreads, so execution and custody choices become even more important there.

Currency and macro considerations

When you buy a yen-priced stock you have two sources of return: the performance of the company in yen, and the FX movement between yen and your base currency. Currency effects can either amplify or offset local equity returns. Japan’s macro backdrop, monetary policy (including the Bank of Japan’s stance) and global yield differentials influence the yen strongly, and investors need to decide whether to hedge currency exposure or accept it as part of the return profile. For long-term investors currency hedging often adds cost and complexity; for short-term or absolute return strategies, active FX management can be essential. Consider how dividends are taxed after FX conversion as well, since conversion timing affects net receipts.

Portfolio construction: weighting Japan inside a global portfolio

How much Japan should you hold? That depends on your diversification aim and what the rest of your portfolio looks like. Japan represents roughly a double-digit share of global market capitalization, so a market-cap aware global equity allocation will naturally include a meaningful Japan weight. Many investors tilt slightly underweight Japan because of sector and currency biases, while others overweight it for value and dividend yield.

Buying Japanese stocks typically weights you toward industrials, autos, electronics, and capital-goods suppliers because those sectors dominate Japanese large-cap indices. That means an allocation to Japan is often an allocation to global manufacturing cycles, export demand and supply-chain technology (sensors, robotics, semiconductor equipment, and similar). Financials and consumer staples add yield and domestic exposure, while pharmaceuticals and select tech/media names provide diversification into longer-duration earnings. Knowing this helps you decide whether a country allocation matches your macro or thematic view.

You can use ETFs for neutral, low-maintenance allocation, and reserve direct stock selection for high-conviction positions where you have done specific fundamental and governance analysis.

Alternatives to buying shares at Japanese exchanges

Direct local shares gives clean exposure, full participation in corporate actions and voting, and the tightest tracking to Japanese fundamentals, but they are not without downsides. For starters, you need a suitable broker for Japanese securities, and you also have to manage JPY conversion risks and Japanese settlement mechanics. To simplify, many foreign investors use ADRs instead, since they are traded on exchanges in the United States. ADRs trade in USD and are convenient, but they can introduce tracking differences and occasionally wider spreads versus the Japanese listing.

Another alternative for investors seeking exposure to Japanese markets are mutual funds or exchange-traded funds (ETFs) with this profile. You can for instance invest in ETFs that tracks the Nikkei 225 or TOPIX. It is less precise than direct stock picking (and ADRs), but for many investors, that is actually a pro and not a con. By picking the right fund for your Japanese investment strategy, you can obtain a diversification from day one, even if you do not have a lot of capital to invest. Funds remove custody and corporate-action friction and are a straightforward way to implement a market-cap or factor tilt without single-name risk.

What is an ADR?

ADRs (American Depositary Receipts) let us buy Japanese company exposure on U.S. exchanges, simplifying settlement and clearing but sometimes widening the spread between the ADR price and the underlying local market due to fees and cross-listing liquidity effects.

ADRs are U.S. traded certificates that represent ownership in shares of a foreign company.

They allow investors to buy foreign stocks easily on U.S. exchanges without dealing with foreign markets or currencies.

How it works: A U.S. bank buys shares of a foreign company. The bank issues ADRs in the U.S. that represent those shares. The ADRs trade on U.S. exchanges in U.S. dollars. Each ADR may represent 1 share, multiple shares, or a fraction of a share.

Example: You are based in the U.S. and want exposure to Toyota. Instead of buying it on any of the exchanges where it is listed (e.g. the Tokyo Stock Exchange or London Stock Exchange), you buy Toyota ADRs listed on the New York Stock Exchange. Dividends are paid to your in U.S. dollars, and the ADRs are traded under U.S. market rules.

So-called sponsored ADRs are issued with the company’s involvement, while unsponsored ADRs are issued without direct company involvement.

Note: Some ADRs are not exchange-listed. Level I ADRs are only available for OTC trading, while Level II and Level III ADRs are listed on exchanges.

Examples of ADRs that give Japanese exposure

- Toyota Motor Corp., Ticker TM, Listed on NYSE. This is one of the most widely held Japanese ADRs.

- Sony Group Corp., Ticker SONY, Listed on NYSE. Sony is an electronics and entertainment giant.

- Honda Motor Co., Ticker HMC, Listed on NYSE. Honda is an automobile manufacturer.

- Mitsubishi UFJ Financial Group, Ticker MUFG, Listed on NYSE. This is the largest Japanese bank.

- Mizuho Financial Group, Ticker MFG, Listed on NYSE. This is a major Japanese bank.

- Sumitomo Mitsui Financial Group, Ticker SMFG, Listed on NYSE. This is a leading banking group.

- Canon Inc., Ticker CAJ, Listed on NYSE. Canon sells imaging and optical products.

- Takeda Pharmaceutical, Ticker TAK, Listed on NYSE. This is the largest pharmaceutical company in Japan.

What is an ETF?

An ETF is an Exchange-Traded Fund. Unlike a conventional mutual fund, the shares of an ETF are listed on an exchange and traded throughout the trading day, in a manner very similar to stock trading. ETFs are available for many different types of exposure, including ETFs that hold a collection of Japanese listed stocks or are designed to track a specific Japanese stock index, such as the Nikkei 225 or TOPIX. Passively managed index ETFs are available with very low expense ratios.

ETFs that track Japanese indices, e.g. the Nikkei 225, TOPIX, or broader MSCI/FTSE Japan indices, can offer an efficient, low-cost way to gain diversified exposure to Japanese stock markets. They avoid many custody headaches, often trade on local exchanges or on major overseas venues, and their tax reporting is usually straightforward in the investor’s home market.

Evaluate the tracking error of any ETF you consider and understand whether it holds securities physically in Japan or uses synthetic replication.

Examples of ETFs that give Japanese exposure

BROAD EXPOSURE

- iShares MSCI Japan ETF (EWJ) – Tracks the MSCI Japan Index (Large & mid cap Japan equities).

- JPMorgan BetaBuilders Japan ETF (BBJP) – Broad exposure to Japanese stocks via the Morningstar Japan Target Market Exposure Index.

- Franklin FTSE Japan ETF (FLJP) – Tracks the FTSE Japan Capped Index with broad Japan exposure.

- iShares MSCI Japan Value ETF (EWJV) – Focuses on value oriented Japanese large & mid caps.

HEDGED ETFs THAT AIM TO REDUCE THE IMPACT OF YEN-TO-USD CURRENCY SWINGS

- iShares Currency Hedged MSCI Japan ETF (HEWJ) – Broad Japan equities with currency hedging.

- Xtrackers MSCI Japan Hedged Equity ETF (DBJP) – Hedged exposure to the MSCI Japan Index.

- WisdomTree Japan Hedged Equity Fund (DXJ) – Focus on Japanese equities with currency hedging overlay.

SMALL-CAP ETFs

- iShares MSCI Japan Small Cap ETF (SCJ) – Tracks MSCI Japan Small Cap Index.

- WisdomTree Japan SmallCap Dividend Fund (DFJ) – Focus on dividend-oriented small caps.

SECTOR-SPECIFIC ETFs

- WisdomTree Japan Hedged Financials Fund (DXJF) – Focus on Financials (banks, insurance & related).

- WisdomTree Japan Hedged Capital Goods Fund (DXJC) – Focus on capital goods & industrial related names.

- WisdomTree Japan Hedged Health Care Fund (DXJH) – Focus on health care (pharma, biotech, health related industries).

- WisdomTree Japan Hedged Real Estate Fund (DXJR) – Focus on real estate and related companies.

Examples of listed Japanese stock companies

Below, we will take a look at a few companies that commonly appear in long-term portfolios because of scale, franchise strength and liquidity. We will briefly touch on why the company matters and what exposure an investor gets by owning the stock.

Beyond the blue chips, Japan houses highly specialism growth companies (precision sensors, industrial automation, niche software and parts suppliers) that can outperform if you identify secular winners. These names can be more idiosyncratic and require operational familiarity with product cycles and export markets. They are good for select allocations but not ideal as the core of a country bet portfolio.

Large-cap, globally relevant names (what many investors call “core”Japan exposure)

Toyota Motor Corporation

Toyota is the nation’s largest industrial champion and the headline auto exporter. Owning Toyota gives you exposure to global autos, hybrid and battery vehicle rollouts, component supply chains and an extensive manufacturing footprint. Its balance of scale, recurring cash flow and diversification into mobility services makes it the single most visible way to take broad Japanese industrial exposure. Toyota typically sits near the top of every market-cap ranking for Japan.

Sony Group

Sony combines entertainment, sensors, and consumer electronics. The PlayStation and media businesses give recurring software and licensing cash flows, while Sony’s image sensors are critical inputs into global smartphone and camera supply chains. That mix makes Sony a hybrid industrial/consumer/tech play and a common choice for investors seeking growth plus some defensive earnings streams.

Nintendo

Nintendo is a large, brand-driven consumer-tech company where hit titles, hardware cycles, and IP monetisation are very important for earnings. It offers a different kind of tech exposure than pure component makers; more media and content upside.

SoftBank Group

SoftBank is a sprawling conglomerate combining telecom assets, a major tech investment arm and a portfolio of venture investments. Equity ownership in SoftBank is effectively a bet on both its core telecom businesses and the success of its global investment platform. Volatility can be high because of marked-to-market exposure to private and public tech holdings.

Mitsubishi UFJ Financial Group / Sumitomo Mitsui Financial Group / Mizuho Financial

Mitsubishi UFJ Financial Group, Sumitomo Mitsui Financial Group, and Mizuho Financial are three separate companies, but they are all huge banking groups, and they are all interesting for investors who seek high market liquidity combined with exposure to domestic financial intermediation and corporate lending. They’re classic value plays when yields normalize and are widely used by investors looking for dividend income and financial-sector sensitivity to the domestic economy.

Keyence

A leader in factory automation sensors and control equipment, Keyence is often a favorite among investors focused on industrial automation and margins. It’s a growthy industrial with strong profitability and exposure to capex cycles across manufacturing.

Tokyo Electron / Daikin / Panasonic / Hitachi / Honda/ Denso

These six companies are all examples of stocks that give core industrial and manufacturing exposure, such as semiconductors and fabrication equipment, HVAC and factory equipment, broad electrical systems, diversified industrial groups and auto components. Together they are a popular way to gain cyclical and capex-sensitive exposure to Japan’s manufacturing base.

Takeda / Astellas / Daiichi Sankyo

The three companies Takeda, Astella, and Daiichi Sankyo are large pharmaceutical and life-sciences enterprises. They are often used to access defensive, dividend-oriented health care exposure with an R&D and product-pipeline risk profile.

Fast Retailing (Uniqlo)

Fast Retailing is a global retail champion headquartered in Japan. It delivers exposure to retail margins, international expansion (it is known as Uniqlo outside Japan), and consumer trends, and is often used for thematic plays on global consumer staples. The businesses model is fast-fashion retail with vertical integration (design → production → retail). Fast Retailing is Japan’s largest apparel retailer and one of the fastest-growing global fashion companies. Its flagship brand, Uniqlo, is known for functional clothing at affordable prices, with a strong emphasis on technology and efficiency in production and supply chain management.

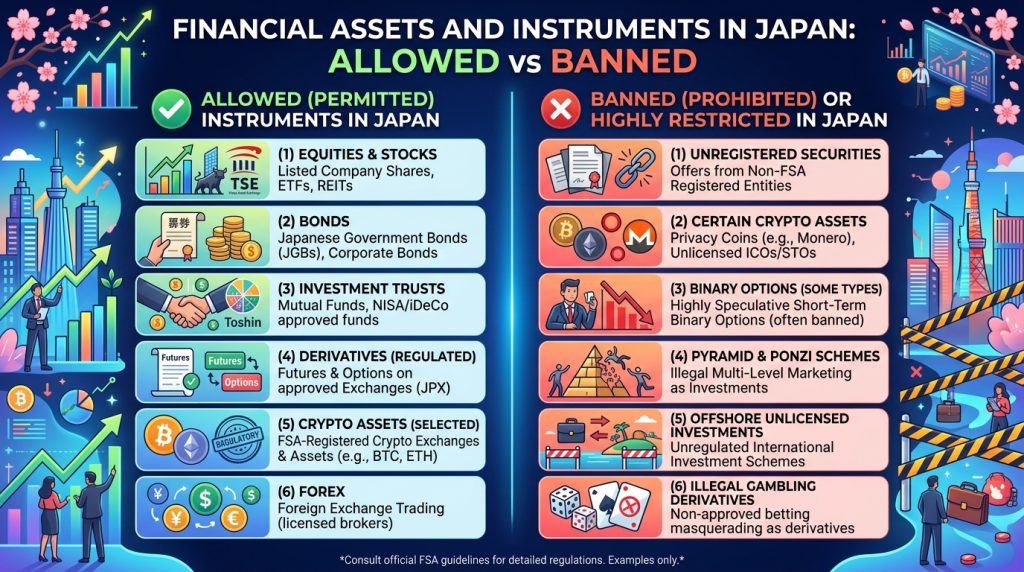

Legality of different types of securities in Japan

We will now proceed to take a closer look at common security and derivative types and how Japan treats them under its regulatory framework.

Japan’s core statutes and supervisory architecture shape whether and how a product may be offered. The Financial Instruments and Exchange Act (commonly abbreviated FIEA) is the central law for securities, derivatives and financial instruments. The Financial Services Agency (FSA) is the primary national regulator; and several industry associations and market infrastructures implement rules and supervision in practice under the FSA framework, including the Japan Securities Dealers Association (JSDA), the Financial Futures Association of Japan (FFAJ) for certain derivatives lines, and the Japan Exchange Group (JPX) for exchange-listed products. When a product is an exchange-listed instrument it follows listing and exchange rules, when it is an OTC derivative it is typically subject to FIEA requirements on dealer registration and reporting. For a subset of designated contracts, there is also mandatory central clearing and platform trading obligations. These basic allocations determine whether an instrument is legal and the practical compliance path for firms that want to offer it. Practically, this means that while many instruments are legal in principle, the ease of legally offering them, and the permissible product design and leverage, varies materially by product and by whether the provider is domestically registered. Observing industry guidance and holding appropriate licenses is essential. Legality in principle does not protect an operator or distributor from administrative sanctions if they ignore the distribution and disclosure obligations that accompany those instruments.

Across instrument types, the same distribution and retail protection rules recur. Firms must register under FIEA or operate as a registered financial institution, segregate client money when required, adhere to capital and reporting standards, provide clear risk disclosure and suitability assessments for retail clients, and comply with anti-money-laundering (AML) obligations. Industry bodies (JSDA, FFAJ) publish product-specific rules, e.g. for CFDs and binary options, that supplement statutory duties.

The FSA and self-regulatory bodies have emphasised consumer protection, transparency and AML compliance in recent years, and the Japanese authorities use public warnings, administrative measures and, where warranted, criminal or civil enforcement to police unauthorized activity and mis-selling. Enforcement attention typically focuses on unauthorized offshore solicitation of Japanese residents, misleading marketing, inadequate client segregation, and complex products sold without appropriate suitability checks. For certain products the regulator and associations have also moved to limit features judged unduly risky and speculative (for example restricting ultra-short expiry retail binaries or imposing strict disclosure and margin standards on OTC leveraged products).

Japan permits a broad spectrum of securities and derivatives, including ETFs, exchange options and futures, OTC swaps, convertibles, warrants, CFDs and even binary options, but the legal permissibly is tightly coupled to registration, disclosure and distribution rules. Exchange-listed products travel the cleanest compliance path, while OTC contracts are permitted but increasingly subject to trade reporting and clearing mandates. Packaged or retail-targeted leveraged products attract the most supervisory scrutiny.

Exchange-traded funds (ETFs)

ETFs are legal, actively traded on JPX (Tokyo), and governed by the usual securities listing rules and investment trust law that apply to listed funds. The exchange treats ETFs much like stocks for trading purposes, subject to exchange rules and book-entry custody through JASDEC. Sponsors must satisfy fund and listing criteria and follow disclosure, NAV calculation, and creation/redemption rules. In practice, Japan supports a broad menu of ETFs (including leveraged and inverse products) and, since recent rule changes, JPX has expanded the types of ETFs that may list. For anyone buying ETFs, examples of main practical considerations are the listing rules, custody/processing through the Japanese book-entry system, and the fund disclosure regime.

Exchange-listed options and futures

Exchange-traded derivative contracts, such as equity options, index options, financial futures, and commodity futures, are legal and listed on recognized venues. These products sit under the exchange and clearinghouse rulebook and are subject to margining, position limits, surveillance, and the FIEA/related regulations. Clearing is typically through a domestic central counterparty. For an investor, this means exchange models offer legal certainty and standardized rules (auction/continuous trading windows, expiry mechanics, clearing house settlement) that differ from bespoke OTC options or structured payouts.

OTC options, swaps, and other bilateral derivatives

OTC derivatives, including plain-vanilla options, interest-rate swaps, credit default swaps, and a wide variety of bespoke instruments are legal in Japan but are regulated as OTC financial derivatives under the FIEA, and where relevant, by the Commodity Futures Exchange Act for commodity-referenced products.

The FSA has introduced mandatory reporting, and the JFSA commissioner has the power to designate particular classes of OTC derivatives for mandatory central clearing and/or specified execution methods. Designated products (for example certain yen interest rate swaps and some credit derivatives) must be cleared at an approved CCP.

Market practice is to use standard agreements (ISDA), document collateral and margining, and comply with trade reporting and clearing obligations where applicable.

Contracts for Difference (CFDs)

CFDs are available in Japan and operate within the same regulatory perimeter that governs other leveraged OTC products. The industry is subject to self-regulatory rules from JSDA/FFAJ in addition to FIEA obligations. Firms that offer retail CFDs must be appropriately registered, segregate client funds, disclose risks, execution and charges, and comply with margin and leverage rules set for retail customers. The FSA and industry bodies actively supervise distribution practices. Because of these rules, many domestic offerings are structured and limited compared with offshore CFD platforms based in lax jurisdictions.

Binary options

Binary options occupy a special place in Japan’s rulebook. Binary-style products are permitted, but tightly regulated under industry rules (FFAJ/JSDA) and FIEA obligations when offered to retail customers. The associations have issued detailed rules to limit excessively speculative structures, including standards for exercise/settlement, disclosure, and platform governance. The FSA periodically issues consumer warnings about the risks of foreign, poorly platforms. Practically, that means onshore, association-member binary products can be lawful if they comply with the self-regulatory and statutory requirements, but there are a lot of restrictions in place, especially when it comes to protecting consumers (retail traders) from the dangers of short-expiry, high-frequency OTC binaries. Retail traders in Japan therefore find regulated Japanese binary offerings much more restricted than what we see on offshore platforms operating from lax jurisdictions.

You can find a binary options broker by visiting BinaryOptions.net. Most brokers offer options based on a number of different large Japanese companies.

Convertible bonds, warrants, and structured notes

Hybrid products such as convertible bonds (corporate debt with an equity conversion feature), warrants, and structured notes are standard securities in Japan and may be issued, listed, and sold under the applicable laws. Convertibles are ordinary debt instruments with conversion rights and must follow corporate bond and securities disclosure rules when publicly offered. Warrants and structured notes are subject to prospectus and suitability requirements when distributed to retail investors. Structured products that embed derivatives elements must be documented to show valuation, risk, and any counterparty exposures, and distributors must observe sales suitability rules and disclosure duties under FIEA. In short, convertible bonds, warrants, and structured notes are legal and widely used in Japan, but their distribution to retail investors draws particular supervisory attention.

Futures, forwards, and commodity derivatives

Financial futures and commodity futures traded on exchanges are legal and listed under exchange regimes with standard clearing and margining. OTC forwards and commodity derivatives are similarly legal, but governed either by FIEA (if they reference financial instruments) or by the Commodity Futures Exchange Act and related rules (if they reference commodities). The market infrastructure for futures is mature. The legal distinction between cash-settled forwards and physically settled trades matters for regulatory classification and how positions are reported and cleared.

Securitised debt, REITs, and collective investment products

Securitised debt, real estate investment trusts (J-REITs), and investment funds are legal and operate under their respective statutes and disclosure regimes. Listed REITs trade on JPX and are subject to REIT law and exchange listing rules. Securitised debt and ABS issuance follow issuer-level disclosure and prospectus requirements. Collective investment schemes are regulated under the FIEA and related trust law, and public offerings require prospectuses and registration or notification depending on the structure. These product types are part of mainstream capital markets activity and are commonly offered to both institutional and retail investors with the usual distribution and disclosure safeguards.